What Is Annual Income? Take-Home, Gross, and Net Income Explained

Published:

Last Updated:

Category: Overcoming Job-Change Anxiety

Published:

Last Updated:

Category: Overcoming Job-Change Anxiety

Authors: Shusaku Yosa

When you hear the word "annual income," do you picture the gross figure, or the money you can actually spend? Some people have been puzzled to find that the annual income in a job posting differs from the amount deposited into their account. This article explains what annual income is, and the difference between "take-home pay," "gross pay," and "income (shotoku)," using concrete examples.

* Tax rates, social insurance rates, and deduction amounts change by fiscal year and with legal revisions. The percentages and estimates in this article are approximate. For exact amounts, check your pay slip and the information from the National Tax Agency and each insurer.

Annual income is the total salary paid by a company over one year (January 1 to December 31). It is the sum of base pay plus overtime pay, various allowances, and bonuses—the "total amount paid" before taxes and social insurance are deducted.

This "total before deductions" has the same meaning as "gross pay," explained next. The annual income shown in job postings and income certificates is basically this gross figure.

The most easily confused terms around annual income are "gross" and "take-home." In short, gross is the amount before deductions, and take-home is the amount after deductions.

Gross is the total payment before taxes and social insurance are deducted. On a monthly basis it is the "gross monthly income (total payment)," and on a yearly basis it is the "gross annual income (= annual income)." On a pay slip, this corresponds to the "total payment" field.

Take-home pay is the amount actually deposited into your account after taxes and social insurance are deducted from gross. The formula is as follows.

Take-home = gross − (social insurance + income tax + resident tax)

Take-home pay is generally about 75–85% of gross as a guideline. Because income tax is progressive—the rate rises as income increases—people with higher incomes tend to have a lower take-home ratio.

The take-home ratio also varies with age (whether long-term care insurance applies), dependents, and the municipality you live in.

What is deducted on the way from gross to take-home falls into two broad categories: "taxes" and "social insurance."

Because resident tax begins from the second year, new members of the workforce sometimes feel their take-home has decreased in the second year compared with the first.

Another term easily confused with "annual income" is "income (shotoku)." Income is a concept used to calculate taxes and differs from annual income itself.

In other words, subtracting deductions in order from annual income (gross) gives employment income → taxable income, and income tax is the tax rate applied to taxable income. The key point is that annual income is not directly the taxable base.

Annual income, take-home, gross, and income look similar but refer to different amounts. Understanding the differences lets you correctly read pay slips and job postings.

You can check your own take-home on your pay slip. Knowing the gap between gross and take-home is also useful for household budgeting and for comparing annual incomes when changing jobs.

A curated selection of resume (rirekisho) templates for job changers. We explain formats by use—including the MHLW stand...

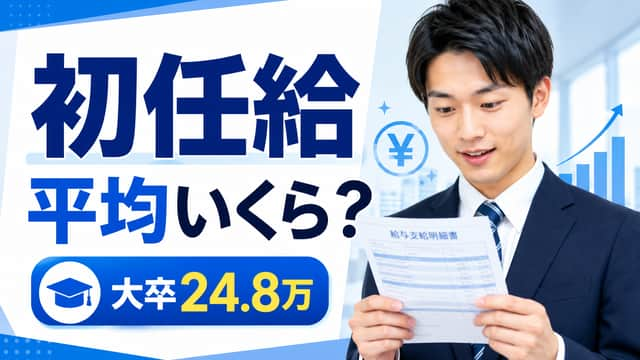

The average starting salary is about 248,000 yen for university graduates, about 198,000 yen for high school graduates, ...

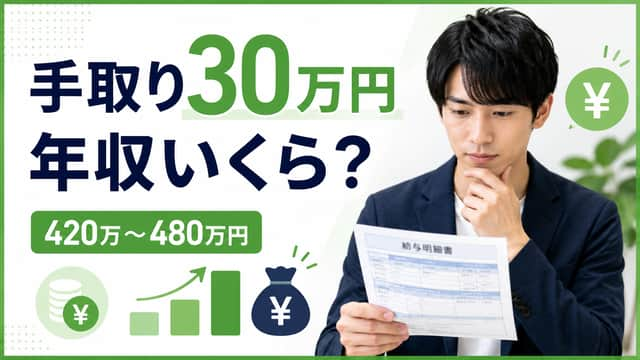

A monthly take-home of 300,000 yen corresponds to a gross annual income of roughly 4.2–4.8 million yen (without bonuses)...